Love and money: Making this couple work

MONTREAL, November 2, 2022 — A new CROP survey for the Chambre de la sécurité financière (CSF) reveals that while Quebecers are pretty comfortable talking about money with their spouse, many factors can create problems when trying to balance love and money.

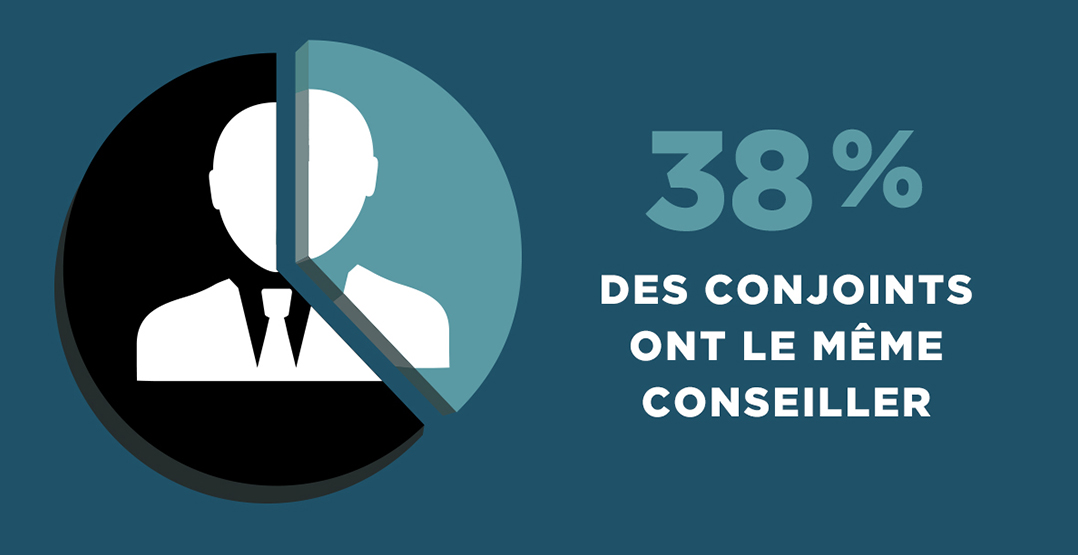

“This survey tells us that 90% of people questioned feel comfortable talking about investments and debt with their spouse, which is excellent news,” stated Marie Elaine Farley, CSF President and Chief Executive Officer, before highlighting the following paradox: “So it’s surprising to learn that half of respondents have never even thought about the consequences of a separation and 74% have never raised the subject with a financial service advisor.”

Key findings of the survey include:

- 57% of people living as a couple pool their incomes for daily life, a proportion that rises to 70% among couples with about the same income.

- 63% of women said that they earn somewhat or substantially less than their partner, while 27% of men say they earn a somewhat or substantially less than theirs.

- About half (52%) said that only one person is mainly involved with financial planning. This proportion is even larger among couples in which one spouse earns more than the other.

- Saving for retirement is mainly done individually (46%). Only 29% of people in a relationship save for retirement with their spouse.

- One fifth (20%) of Quebecers have nothing saved for their retirement.

- More than a quarter of Quebecers in a relationship (27%) report putting money aside deliberately and secretly, without their partner knowing. This behaviour is much more frequent (56%) among people who are financially very comfortable.

- Personal debt is a substantial cause of anxiety, which is worsened when income levels differ. Almost six in ten spouses (57%) feel stressed because of their personal debt and 41% say they feel anxious because of their partner’s debt. Anxiety levels are higher among the more affluent and in people earning less than their partner.

Analysis of the survey

Thanks to collaboration between the CSF and the Institut national de recherche scientifique (INRS), Hélène Belleau, Ph. D., sociologist and INRS professor, participated in the analysis of the survey. She emphasized that “Money is what we call a ‘total social phenomenon’, meaning that it is everywhere in our society and conditions all our relationships and decisions throughout our lives.” Through her research, she has noted that few spouses discuss the organization of their finances and the impact this could have on their savings in the medium and long term. Often, disparities grow without the spouses paying attention. This means that, while financial harmony seems to rule in the majority of Quebec couples, due to the wage gap between men and women, the price of family life weighs much heavier on women if a split up occurs and they are not married.

Professor Belleau concluded from the survey results that, generally, the person with the higher income is the one who takes care of long‑term planning. Among the reasons mentioned by respondents to explain this situation, she noted that the fact one of them “knows more about it” is not connected to gender: the higher income earner, whether a man or a woman, systematically declares they know more about finances than their spouse. She also noted that 21% of respondents think their spouse discourages them from being involved in more long‑term financial planning.

Ms. Belleau also observed that four couples in 10 (42%) do not combine their incomes and instead divide expenses. “In situations where income differences are substantial, even if spouses opt to split the bill proportionally based on each partner’s income, expenditures will weigh more heavily on the person earning less. For example, the choice of purchases is often based on the income level of the person earning more, which will put their partner at a disadvantage because they will be living noticeably beyond their means,” she explained.

“We don’t have data on why certain categories of people are more likely to stash money in secret, and there certainly may be good reasons to do so. However, it is clear that some may be trying to prepare for the economic consequences of an eventual break‑up,” concluded Ms. Belleau.

Role of the Chambre de la sécurité financière

In light of these survey findings, it is important for the CSF to inform its members of the financial dynamics that may exist within couples. Ms. Farley notes that advisors overseen by the CSF have the obligation to really know their clients and look after their best interests. The public should “feel free to discuss any and all of these questions with an advisor, who must offer financial products and services that truly meet the needs and objectives of his or her clients, whether for financial planning, saving or financial security,” indicated Ms. Farley.

To learn more about the many ways in which the CSF protects the public, go to chambresf.com/en.

Download the complete survey results here (in French only).